122 / 172

122 / 172

Atul Ltd | Annual Report 2015-16

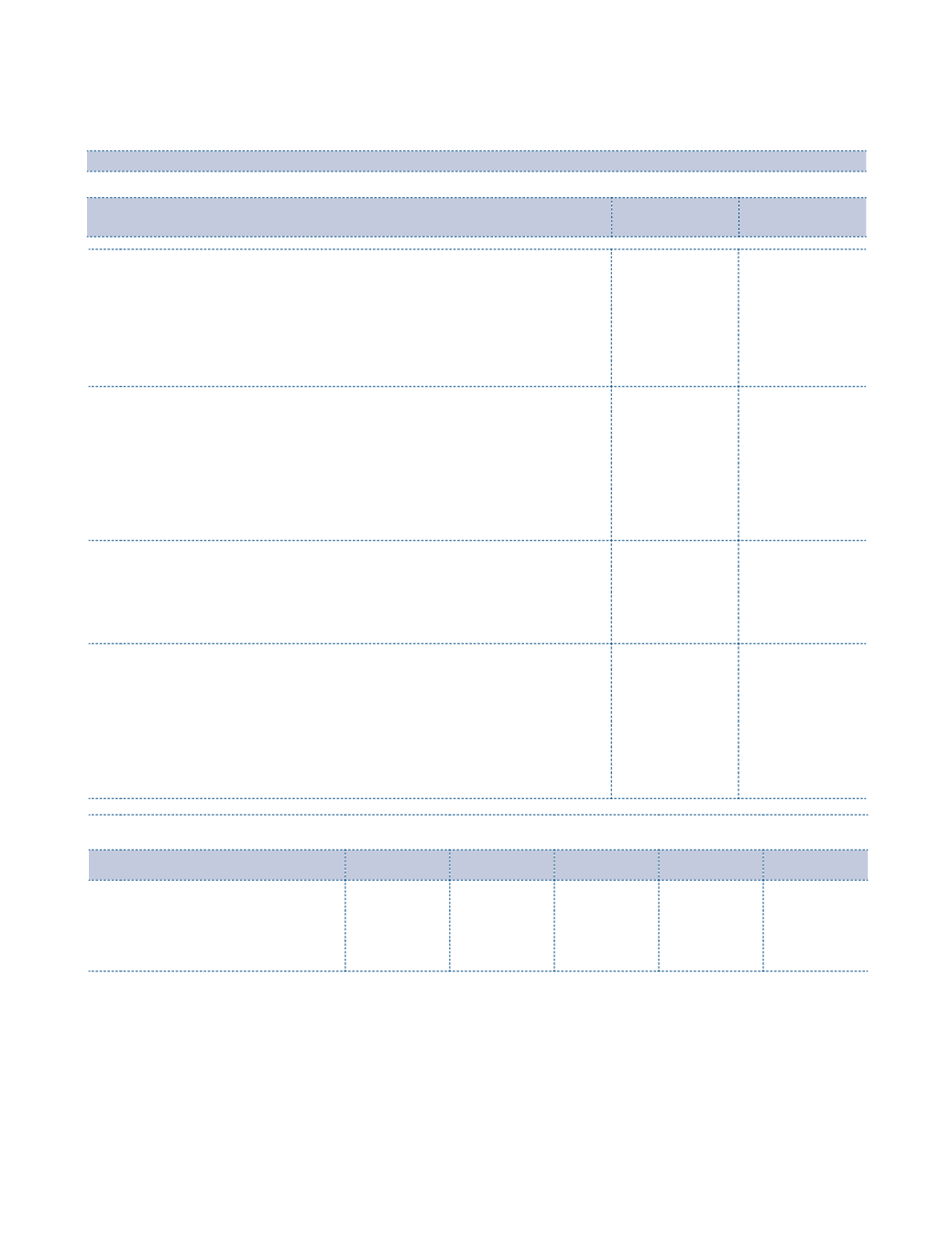

3 Reconciliation of present value of the obligation and the fair

value of plan assets and amounts recognised in the Balance

Sheet:

a) Present value of the defined benefit obligation at the end of the year

(47.27)

(44.44)

b) Fair value of plan assets at the end of the year

47.27

44.44

c) Net liability recognised in the Balance Sheet

–

–

4 Gratuity cost recognised during the year:

a) Current service cost

2.10

2.27

b) Interest cost

3.55

3.88

c) Expected return on plan assets

(3.55)

(3.63)

d) Actuarial loss

3.06

0.23

e) Total expense

5.16

2.75

5 Actuarial assumptions:

a) Discount rate

7.80%

7.99%

b) Rate of return on plan assets

7.80%

7.99%

c) Salary escalation rate

7.75%

7.75%

6 Net asset | liability recognised in the Balance Sheet

Defined benefit obligation

47.27

44.44

Plan assets

47.27

44.44

Deficit | (Surplus)

–

–

Experience adjustments in plan liabilities

1.91

(1.66)

Experience adjustments in plan assets

(0.79)

1.90

Experience adjustments

(

`

cr)

Particulars

2015-16 2014-15 2013-14 2012-13 2011-12

Experience adjustments on:

1 (Gain) | Loss on plan liabilities

1.91

(1.66)

0.40

1.35

(0.01)

2 (Gain) | Loss on plan assets

(0.79)

1.90

(0.06)

(0.29)

1.80

The Company expects to contribute

`

3.94 cr to Gratuity Fund in the year 2016-17.

b) Defined contribution plan:

Amount of

`

9.00 cr (Previous year:

`

8.48 cr) is recognised as expense and included in the Note 25 ‘Contribution

to Provident and Other funds’.

c) Provident Fund liability:

In case of certain employees, the Provident Fund contribution is made to a trust administered by the Company.

In terms of the guidance note issued by The Institute of Actuaries of India, the actuary has provided a

valuation of Provident Fund liability based on the assumptions listed below and determined that there is no

shortfall as at March 31, 2016.

Notes

to the Financial Statements

Note 28.11 Employee benefits

(continued)

(

`

cr)

Particulars

2015-16

2014-15

Gratuity

Gratuity