197 / 220

197 / 220

195

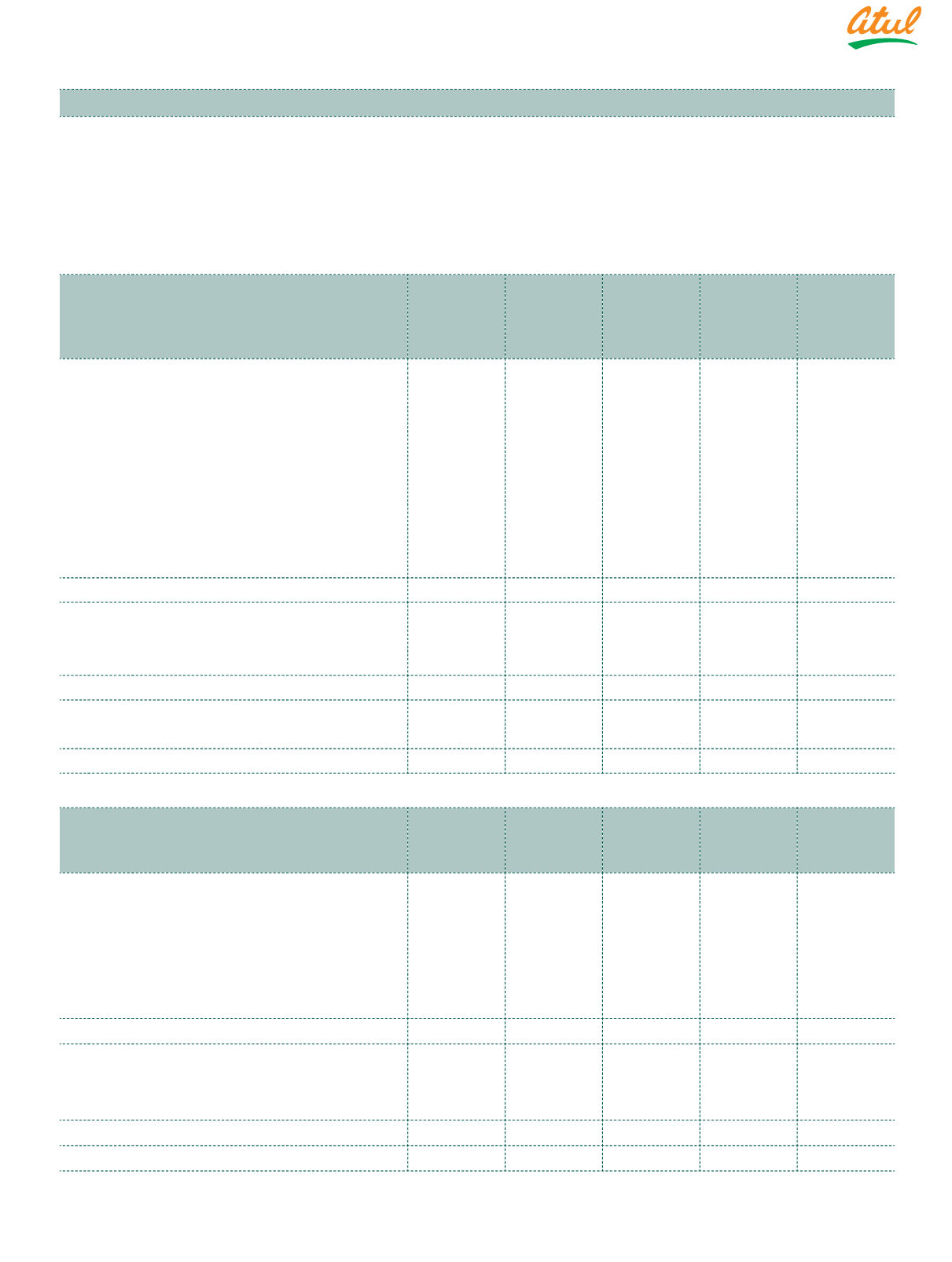

a) Fair value hierarchy

This section explains the judgements and estimates made in determining the fair values of the financial instruments that

are a) recognised and measured at fair value and b) measured at amortised cost and for which fair values are disclosed in

the Consolidated Financial Statements. To provide an indication about the reliability of the inputs used in determining fair

value, the Group has classified its financial instruments into the 3 levels prescribed under the Indian Accounting Standard.

An explanation of each level follows underneath the table:

(

`

cr)

i)

Financial assets and liabilities

measured at fair value - recurring

fair value measurements at March

31, 2018

Note

Level 1

Level 2

Level 3

Total

Financial assets

Financial investments at FVPL:

Mutual funds

11

5.70

–

–

5.70

Financial investments at FVOCI:

Quoted equity shares

6

452.49

–

–

452.49

Unquoted equity shares

1

6

–

–

0.81

0.81

Share application money

6

0.01

–

–

0.01

Derivatives designated as hedges:

Foreign exchange forward contracts

–

0.07

–

0.07

Total financial assets

458.20

0.07

0.81

459.08

Financial liabilities

Derivatives designated as hedges:

Currency options

–

0.02

–

0.02

Total financial liabilities

–

0.02

–

0.02

Biological assets

Tissue culture raised date palms

–

22.70

–

22.70

Total biological assets

–

22.70

–

22.70

(

`

cr)

ii)

Assets and liabilities for which fair

values are disclosed at March 31,

2018

Note

Level 1

Level 2

Level 3

Total

Financial assets

Investments:

Government securities

6

0.01

–

–

0.01

NHAI bonds

6

0.10

–

–

0.10

Security deposits for utilities and

premises

8

–

–

1.48

1.48

Total financial assets

0.11

–

1.48

1.59

Financial liabilities

Borrowings

17

–

–

15.91

15.91

Security deposits

18

–

–

22.46

22.46

Total financial liabilities

–

–

38.37

38.37

Investment properties

3

–

–

141.00

141.00

Notes

to the Consolidated Financial Statements

Note 29.7 Fair value measurements

(continued)